Are you an engineer? What do you think about the value of your job?

How can we get the value of engineering in a company? Or how can we calculate

Intellectual property or royalty rate of a company?

To analyze some financial cases, we have to calculate the

intellectual property of the company in additional to look at the book value on

balance sheet.

Please see the case of "Yeats Valves and Controls

Inc.". The end of first page of this case, Porter said:

"YVC's prospects are brighter than ever. You have technology to die for.

With our intellectual property and new products

coming along, there is a lot of hidden value in this company that's

not

reflected on the balance sheet. Be a realist about the value"

There are many papers and references

to measure the intellectual property of a company. In this article, I chose a

very fascinating hand book which presents six different methods to price the intellectual property of early-stage

technologies.

The reference is as follows:

"ipHandbook of Best Practices"

Chapter 9.3 (2007) titled: "Pricing the Intellectual Property of

Early-Stage

of Basic Valuation Technologies: A Primer

Posted on below link:

Even though I can say to you that above reference is very useful

and interesting materials, there are

some mistakes taken on method of Discounted Cash-Flow Analysis (method IV) and

Table 14. For instance, when you read this method, you cannot still calculate the

royalty rate. Your big question is: How has the royalty rate (12.6%) been

calculated?

The purpose of my article is to improve and to explain the true

method of Discounted Cash-Flow Analysis for calculating the royalty rate.

What should the items be improved?

1. Mistakes on calculations

2. The lack of enough information

3. The lack of good explanations

Let me start by the mistakes on calculations:

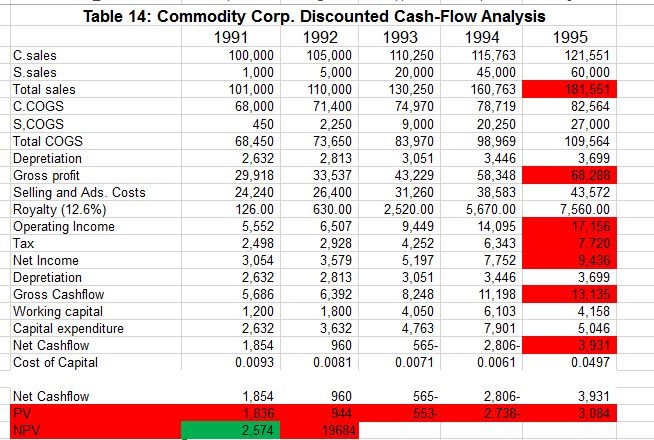

Here is Table 14:

As you can see, the calculation of all present values and total

sales in 1995 are wrong. I corrected them on below spread sheet (Red highlights

are true values):

2. The lack of enough information

When you start a discounted cash flow analysis, you should consider

a terminal value for the end of your period. Because you have not the infinity cash in or cash out. Therefore, you should terminate and close your analysis by

evaluating the value of your business in the end of the period. The formula for

calculating Terminal value is as follows:

Terminal Value =

Free cash flow in the end of period * (1- terminal growth rate %) /

(Cost of Capital % - terminal growth rate %)

For this analysis, I consider 2% for terminal growth rate. Please

see my calculation of terminal value and also NPV on below spread sheet:

3. The lack of good explanations

The most important part of this article is, to calculate the

royalty rate. The above reference do not show us how we can get the royalty

rate equal to 12.6%.

Let me tell you the method as follows:

- At the first, you should eliminate amounts of Specialty product

sales, Cost of specialty product sales and Royalty payment at 12.6% on your

spread sheet and then calculate NPV just like below cited (Yellow highlights):

- In final step, you should add above amounts again and apply the

sensitivity analysis for the royal rate and NPV in which NPV in both step are

the same, it shows you percentage of the royalty rate as follows:

As you can see, the royalty rate is not 12.6% but it is equal to

55%.