Following to article of "A Template for

Financial Section of a Business Plan" posted on link: http://emfps.blogspot.com/2016/08/a-template-for-financial-section-of.htm,

the purpose of this article is to

develop and improve previous template. So, I am willing to introduce you a new ratio

(S) extracted from some new theorems in mathematics in

which by using this ratio, we will be able to focus on only one assumption and

eliminate other assumptions for our analysis. In fact, by changing other

assumptions, this ratio (S) always stays the constant.

Developing of Previous Template

In

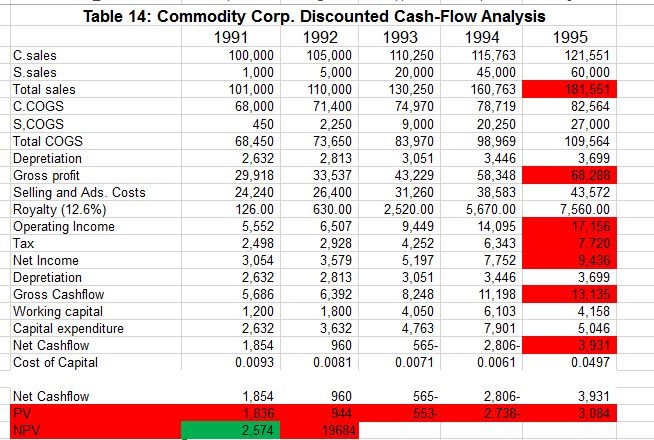

previous template, we had only one column for our assumptions. It means, by

changing a variable (assumption), the changes for all years are the same. For

instance, if we change the growth of sales from 4% t0 6%, the NPV shows us a

growth of 6% for year 1, year 2, year 3 and so on. Please see

below pic

In reality, there is not the same growth for all

years. Therefore, I added other cells on my spreadsheet where we will have a

set of assumptions for each year. This gives us the opportunity for better

analysis by using the Monte Carlo method. Please see blow pic:

The Improve of Previous Template

In new template, I added new assumption which is the Tax rate. In previous template, we have a big

problem when EBTI is negative because we have already added tax payment to net

income. In this case, there is the concept which is named NOL.

What is NOL? It is Net Operating Loss in which we can deduct our NOL

from the taxes we paid in prior years and get a refund, or we can apply it to

future years to lower our tax bill.

This

will help us to recover some net operating losses but usually not all.

The

concept of NOL is the complicated and you cannot easily claim your NOL. Some

people believe to deduct entire NOL from future taxes (Tax loss carry forwards)

or to add tax payment to net income when EBTI is negative (my previous

template). Let us see below example:

Assume

Company X has net

sales of $2,000,000 but expenses of $2,200,000.

Its net operating loss is $2,000,000 - $2,200,000 = -$200,000.

Company

X will probably not have to pay taxes that year, because it has negative taxable income. But let's assume that next year,

Company X makes more sales and records $700,000 of taxable

income. Company X pays a corporate tax rate of 40%.

Normally,

the company would need to pay $700,000 x 40% = $280,000 in taxes. But

because it had a tax loss carry forward from last year, it can apply last year's

loss to this year's tax bill, reducing it significantly (or even to $0,

depending on the jurisdiction Company X is in).

Let's

assume that Company X can apply the entire -$200,000 tax loss carryforward to

this year's tax bill. Instead of owing $700,000 x 40% = $280,000 in taxes,

Company X now owes only ($700,000 - $200,000) x 40% = $200,000 in taxes.

But other

people say another story as follows:

"It's

rare to see a company acquired for the purpose of NOLs today (at least through

a direct acquisition). This is because of 382 limitations on the usability of

NOLs in the case of a change in control of a company's equity rendering your

NOLs almost worthless on a present value basis. NOLs are currently limited to

3.98% of the value of the company during a change of control. This number is determined

by the IRS monthly and (along with the value of the company for 382 purposes)

will be fixed at the time of the change of control. Based on your business and

applicable tax laws, you may also have to distinguish between cash taxes and

accounting taxes. The actual formula for NOI after taxes is simply: NOI -

taxes. This is equivalent to (1-taxes) * NOI if your taxes are positive, but

should be just NOI since your taxes are zero if your NOI is negative."

Therefore, we

have the pessimistic and optimistic comments. Anyway, I choose the pessimistic

situation because here is a good opportunity for our

analysis as follows:

For obtaining

zero taxes on my spreadsheet when NOI is negative, I use a simple trick in

which I add one row under item of tax payment (Adjusted tax payment) by below

formula on all months and years of cash flow statement:

=IF (B36>0;

B36; 0)-B36

Please see below pics:

In this case,

if your tax payment is negative, adjusted tax payment will be positive where

the total sum is zero. But if your tax payment is positive, adjusted tax

payment will be zero.

Then, on

spreadsheet of Income statement, I add tax payment and adjusted tax payment.

But what is

good opportunity?

Above trick

gives us a good opportunity on our analysis. If we change the tax rate for each

year but NPV, IRR and also Enterprise value do not change, it means that the

combination of other assumptions presents net operating loss in its year. For

example: you can see when I change tax rate in year 4 and year 5, NPV does not

change. Therefore, we have net losses in year 4 and year 5. (Please see below

pics)

A New Ratio (S)

Now, let me introduce you a new ratio that if you apply it on each

assumption, by changing other assumptions this ratio always stay the constant.

Example:

I consider Cost of Capital as base of assumption to generate this

new ratio. Of course, we can choose any assumption as the base of calculation

this ratio.

- First, I use form a sensitivity analysis for the Cost of capital

and NPV. (see below pic)

- Then, the ratio of "S"

is equal to NPV 3 minus NPV 2 divide NPV 4 – NPV 1

S = (NPV3 – NPV 2) / (NPV 4 – NPV 1)

We can use from IRR and also Enterprise value instead NPV.

In below pic, you can see the ratio of "S" has been calculated

by using above formula for all assumptions:

Now, I change all assumptions except the Cost of Capital in below

pic:

As you can see, the ratio of "S" will stay the constant

for all changes of assumptions.

Indeed, what is application of the ratio of "S" for our

analysis?

For answering to above question, at the first we should familiar to

a new theorem of mathematics which is the rule of 0.333333….

Then we can start our analysis by using the Monte Carlo Method.

Of course, there is another ratio which is named ratio of "P". This ratio has also the property just like ratio of "S" where by changing all assumptions ratio "P" stays the constant. The formula for ratio "P" is as follows:

Of course, there is another ratio which is named ratio of "P". This ratio has also the property just like ratio of "S" where by changing all assumptions ratio "P" stays the constant. The formula for ratio "P" is as follows:

P = (NPV 2 – NPV1) / (NPV3 – NPV2) or

P = (EV2 – EV1) / (EV3 – EV2) or

P = (IRR2 – IRR1) / (IRR3 – IRR2)

Please see below pic:

Now, I change all assumptions and you can see ratio "S"

and "P" stay the constant. Please see below pic:

Are there other ratios which have the same property?