The purpose of this article is to generate new theorems of

probability and to find out some applications of these theorems. In this case,

suppose that we have a covered basket that contains many dices. In many blind

tests, we will reach in and pull out a dice and set it on the table on one row

from left to right. It is clear, each dice has six events (choices) including

1, 2, 3, 4, 5, and 6.

Theorem (1): Rule of fifty plus (50 %+)

I start this theorem by using three dices. At the first, I pull out

one dice from basket then second dice and finally third dice and set them on

the table on one row from left to right.

The question is: What is the

probability for number of third dice less than or equal to average of numbers

first and second dices?

Let us have the dices as follows:

D1 = first dice

D2 = second dice

D3 = third dice

D1 D2 D3

I am willing to know:

P (D3 ≤ ((D2 + D1) / 2)) =?

Definitely, we have 6^3 = 216 permutations with repetition.

We can calculate the probability equal to 54. 1667%.

P (D3 ≤ ((D2 + D1) / 2)) =

54.1667%

Or, what is the probability for number of third dice more than or

equal to average of numbers first and second dices?

The answer is the same:

P (D3 ≥ ((D2 + D1) / 2)) = 54.1667%

Now, another question is: What is the probability number of third

dice less than or equal to twice number second dice minus first dice?

P (D3 ≤ ((2*D2) - D1)) =?

The calculation shows us that the probability is the same equal to

54. 1667%

P (D3 ≤ ((2*D2) - D1)) = 54.1667%

Therefore, we can say:

P (D3 ≤ ((D2 + D1) / 2)) = P (D3 ≥ ((D2 + D1) / 2)) = P (D3 ≤

((2*D2) - D1))

Let me expand this idea as follows:

If we assume all dices contains infinity numbers which are members

of Real Number as follows:

D1 and D2 and D3 are subsets of Real Number

In this case, each dice is included a set of Real Number in which

the numbers of sets will be different, then we will have:

P (D3 ≤ ((2*D2) - D1)) > 50%

I name this theorem: The rule of fifty plus (50 %+)

What are the

applications?

Here I have brought an example of financial management.

Let me again refer you to my article of "A Template for

Financial Section of a Business Plan (Con)"

posted on link:

http://emfps.blogspot.com/2016/08/a-template-for-financial-section-of_25.html

posted on link:

http://emfps.blogspot.com/2016/08/a-template-for-financial-section-of_25.html

We can apply this theorem to predict assumptions when we have the

final reports of previous years

by probability of more than fifty percent (50 %+) for instance, I utilize this theorem for growth rate of sales as follows:

by probability of more than fifty percent (50 %+) for instance, I utilize this theorem for growth rate of sales as follows:

If we replace the dices by years of sales (Income statement) and

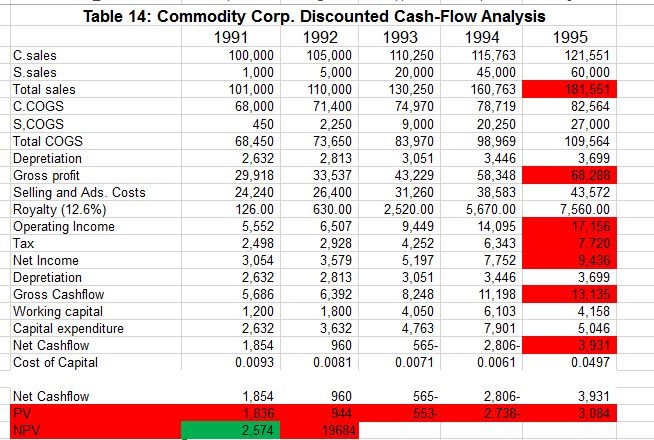

use from Monte Carlo method to iterate calculations, we will reach to the rule

of 50 %+. (Please see below pic)

On above spreadsheet, we have sales for year 3, 4 and 5. Then I use

different probability distribution and different growth rate for CUT OFF. By

one way data table, you can see an average of P (x) is equal to 53.9% by

standard deviation of 0.000499.

P (x) = P (year5 ≤

((2*year4) – year3)) = 53.9%

It means that there is a probability more than 50% in which sales

in year 5 will be less than or equal to twice sales in year 4 minus sales in

year 3.

You can check this theorem (50 %+) for all income statements,

annual reports and so on.

Even though we have found out this theorem, there is still more

than 40 % risk to use this theorem. But, how can we decrease the risk of

projection for assumptions or increase the probability prediction of our

assumptions?

For deducting this risks, we have to generate other theorems by

increasing the number of dices or changing the functions.