Following to previous article posted on link: http://emfps.blogspot.com/2016/09/the-generating-new-probability-theorems.html, you can review second theorem as follows:

Theorem (2): Rule of sixty plus (60 %+)

I start theorem (2) just like theorem (1) by using three dices but

I change the function to a Transcendental function.

As we know, there are two types of functions in mathematics

(Calculus). The first functions are named Algebraic function. These ones are

the functions which are applied in below equation:

0 = ( Pn (x)y^n +...P1(x)y + P0 (x

......... (Where P0 (x), P1(x

Pn (x) are the polynomials of "x

......... (Where P0 (x), P1(x

Pn (x) are the polynomials of "x

I used Algebraic function for theorem (1).

Second functions are named Transcendental function including two

group: 1) Trigonometric function 2) Exponential function. These functions are

not compatible with above equation.

In theorem (2), I will apply a type of trigonometric function.

Assume we again set three dices on the table in one row from left

to right. We will have:

Dice1 Dice2 Dice3

Now, consider three dices as three variables as follows:

Dice1 = x, Dice2 = y,

Dice3 = z

I am willing to define function f (x, y) below cited:

z = f (x, y) = x + COS y

We know the domain of "x" and "y" is the same

the range of "z" equal to 1, 2, 3, 4, 5 and 6.

I am willing to know, what is below probability:

P (z <= x + COS y) =?

We can calculate the probability which is exactly equal to 50.00 %.

P (z <= x + COS y) = 50.00 %

Now, I will pull out another dice from basket and add forth dice on

the table right side of dice 3. We will have Dice 4 and I will assign variable

"w" to this dice:

Dice 4 = w

Suppose the function will be:

w = f (x, y, z) = x + COS (y + z)

What is below probability?

P (w <= x + COS (y + z)) =?

We have 6^4 = 1296 permutations with repetition.

The probability is again calculated exactly equal to 50.00 %.

P (w <= x + COS (y + z)) = 50. 00%

Then, I will pull out another dice from basket and add fifth dice

on the table right side of dice 4. We will have Dice 5 and I will assign

variable "t" to this dice:

Dice 5 = t

Suppose the function will be:

t = f (x, y, z, w) = x + COS (y + z + w)

It is clear, permutations with repetition is equal to 6^5 = 7776 and

the probability will again be 50%.

P (t <= x + COS (y + z + w)) = 50%

Finally, I will pull out another dice from basket and add sixth

dice on the table right side of dice 5. We will have Dice 6 and I will assign

variable "r" to this dice:

Dice 6 = r

Suppose the function will be:

r = f (x, y, z, w, t) = x + COS (y + z + w + t)

What is below probability?

P (r <= x + COS (y + z + w + t)) =?

Permutations with repetition is equal to 6^6 = 46656 and the

probability is again 50%.

P (w <= x + COS (y + z +

w + t)) = 50%

Therefore, we can reach to a general theorem in which there are

"n" dices:

If we have "n" dices with below function:

xn = f (x1, x2, x3, ……..xn-1) = x1 + COS ( x2 + x3+ …..

xn-1)

Then, below Probability will be 50%:

P(xn <= x1 + COS (x2 + x3+ ….. xn-1)) = 50%

What is the application of theorem (2)?

Let me again refer to my article of "A Template for Financial

Section of a Business Plan (Con)"

posted on link:

If you want to test these theorems and see real

application of these theorems in the field of financial management

you should select 10, 20, 50 or more companies and apply

these theorems on growth rate of sales and costs or amount of sales and costs in the sequential years, quarters and so on.

Here, I have bought an example for 20 company that I have covered the names. You can follow me as

follows:

Step 1: Select 20 companies

in different industries

Step 2: Go to Google finance and search name of each company

Step 3: For each company click on Financials (left side of page)

Step 4: Copy total revenue and cost of revenue for five sequential

period of 13 weeks and paste on excel spreadsheet

Step 5: Calculate growth rate for total revenue and cost of revenue

Step 6: Calculate the function of theorem (2) for two sequential

period of 13 weeks and compare it with third sequential period of 13 weeks

Step 7: Calculate the probability

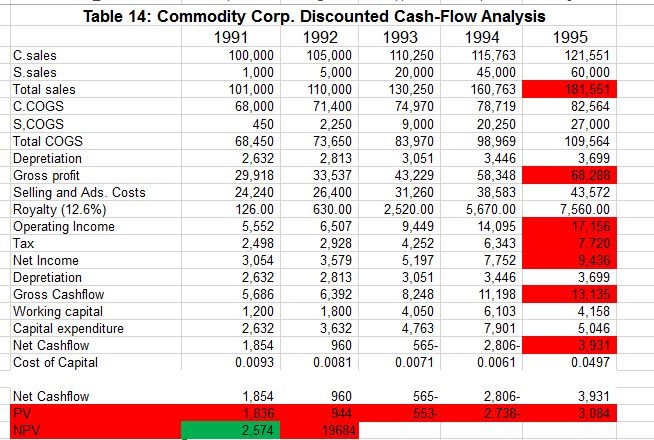

You can see Figure (1) which is my example:

( 1) Figure

In my example, I am predicting the periods of 13 weeks ending 2016-

03 – 26 and 13 weeks ending 2016 – 06 – 25. You can see, for function of z = x

+ cos y, the probability is exactly 100% for both periods (for revenue and

cost). It means that the predictions are 100% true. But these predictions are

not useful because they show us very high upper stream line. It is just like, I

say to you that the sales will not increase more than 150 or 200% for the next

period. Therefore, there are two important questions

1. Why is there the significant difference between the probability

of theorem (2) and real probability which is 100% instead of 50%?

2. How can we decrease upper stream line where the predictions will

be useful for us?

Answer to question (1):

As we can see, the growth rates usually are between -100% to + 100%

(-1 to +1).

Therefore, let me consider all

dices contains infinity numbers which are members of Real Number between -1 to

1 as follows

D1 =

{x │ x ϵ R,

-1< x <1}

= D2

{y │ y ϵ R,

-1< y <1}

= D3

{z │ z ϵ R, -1<

z <1}

Now, if we use above conditions and apply Monte Carlo method for

our analysis, we will find that the probability for theorem (2) will increase

to more than 85% with Average approximately 85% by standard deviation of 0.001.

Please see Figure 2

Figure (2)

Answer to question (2):

Only way to decrease upper stream line is, to divide function of

theorem (2) to some numbers. For instance, I apply the Monte Carlo analysis for

below functions:

z = f (x, y) = (x + COS (y)) / 4

According to Figure (1), the probabilities are 95% and 85% for my

example. In the reference with Monte Carlo analysis, we can say:

P (z <= (x + COS y) /4) > 65%

with Average > 64 % and standard

deviation approximately 0.0015

z = f (x, y) = (x + COS (y)) / 6

Figure (1) shows us, the probabilities are 95% and 72.5% for my

example. Regarding to Monte Carlo analysis, we can say:

P (z <= (x + COS y) /6) > 60%

with Average approximately 60 %

and standard deviation 0.0018

Since theorem (2) divided to 6 is more useful for us, I can say that

the Rule of sixty plus (60 %+) is as follows:

P (z <= (x + COS y) /6) > 60%